Understanding Crypto Ban in India

No person shall mine, generate, hold, sell, deal in, issue, transfer, dispose of or use Cryptocurrency in the territory of India.

The above is the first clause in the draft of a bill called Banning of Cryptocurrency & Regulation of Official Digital Currency Bill, 2019 issued by the Department of Economic Affairs, Government of India. The proposed bill is considered as a final nail in the coffin for any sort of cryptocurrency trading in India, and has resulted in several petetions being filed in the Supreme Court of India from crypto-exchanges in India. Notwithstanding lesser extent of awareness about cryptocurrencies in India, there were still 5 million digital currency holders in India. Further, the worst to face would be the entrepreneurial organisations who had set up mining infrastructure for mining cryptocurrencies. The heavy investments they made have now become completely useless as the mining computational machinery, being specialized for particular tasks, cannot be used for other computational purposes. There has been stringent criticism that the failure of the government and RBI to regulate has hampered the rise of such an innovative technology which is being widely accepted by nations worldwide.

The Reserve Bank of India (RBI) had given warnings several instances before the ban was actually laid out. The main concern of the government seems to build a regulatory framework for private currencies. This is because most tracking cryptocurrencies to their owners is very difficult with the privacy and security guarantees of crypto in place. One segment of experts believe that levying tax on each transaction would be the way to regulate crypto. Here, again the question of determining the origin of transactions remains unsolved. The possibility of terror funding in crypto is another thing which might be of prime concern to the government. The government states that only government-owned digital currency could be introduced. It, however, creates ambiguity about the decentralized nature of such government-backed digital currencies. The draft also mentions that the use of the distributed ledger technology for applications other than those involving trading of private cryptocurrencies is allowed. Although this does not restrict the application of blockchain in different areas, it is still not clear what would be the exact relaxations and restrictions on use of blockchain technology, pertaining to the vast extent possibilities blockchain opens up for businesses and otherwise. All in all, it would be shameful if India just shuts doors to innovation and technology

without putting efforts in trying to build a regulation for it.

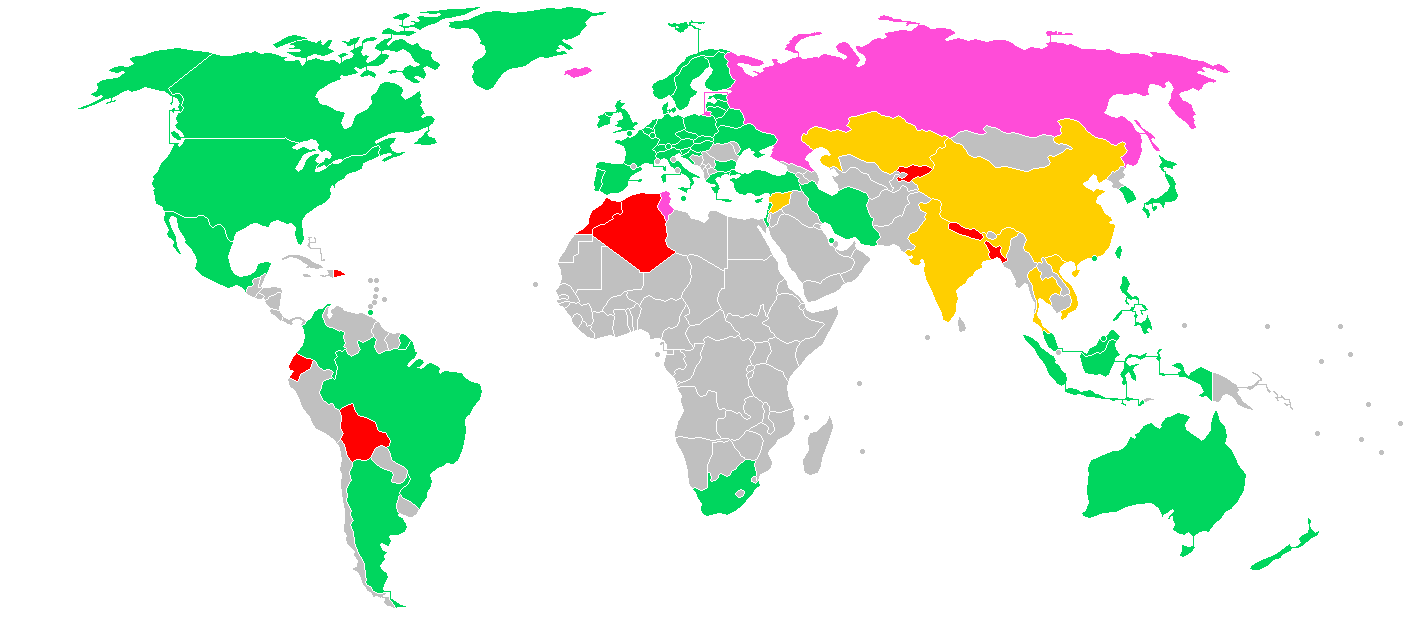

Many developed as well as developing economies have well-adopted to the rising digital currency markets1. Japan has allowed the use of crypto with a proper legal system regulating cryptocurrency trading2. Singapore become the second country in the world after the US to regulate virtual currencies such as bitcoins long back in 20143.

Permissive (legal to use bitcoin)

Contentious (some legal restrictions on usage of bitcoin)

Contentious (interpretation of old laws, but bitcoin is not prohibited directly)

Hostile (full or partial prohibition)

The benefits of decentralized economy are immense and blockchain technology promises to bring about a drastic change the way economies and trading work. Malpractices are a part and parcel of each disruptive technology. It is on the will and determination of the law-makers to ensure responsible and legal use of such technologies and bring about the benefits to the common. It sure might take some time, but India too would adopt a robust regulatory framework for cryptocurrencies and pave a way for a decentralized economy.